.svg)

Are equity investors being adequately compensated for the risk they're taking?

The Shiller Excess CAPE Yield (ECY), the projected real-return pickup from owning the S&P 500 over 10yr treasuries, now sits firmly in the bottom quartile of the past 50 years.

A few additional data points worth considering:

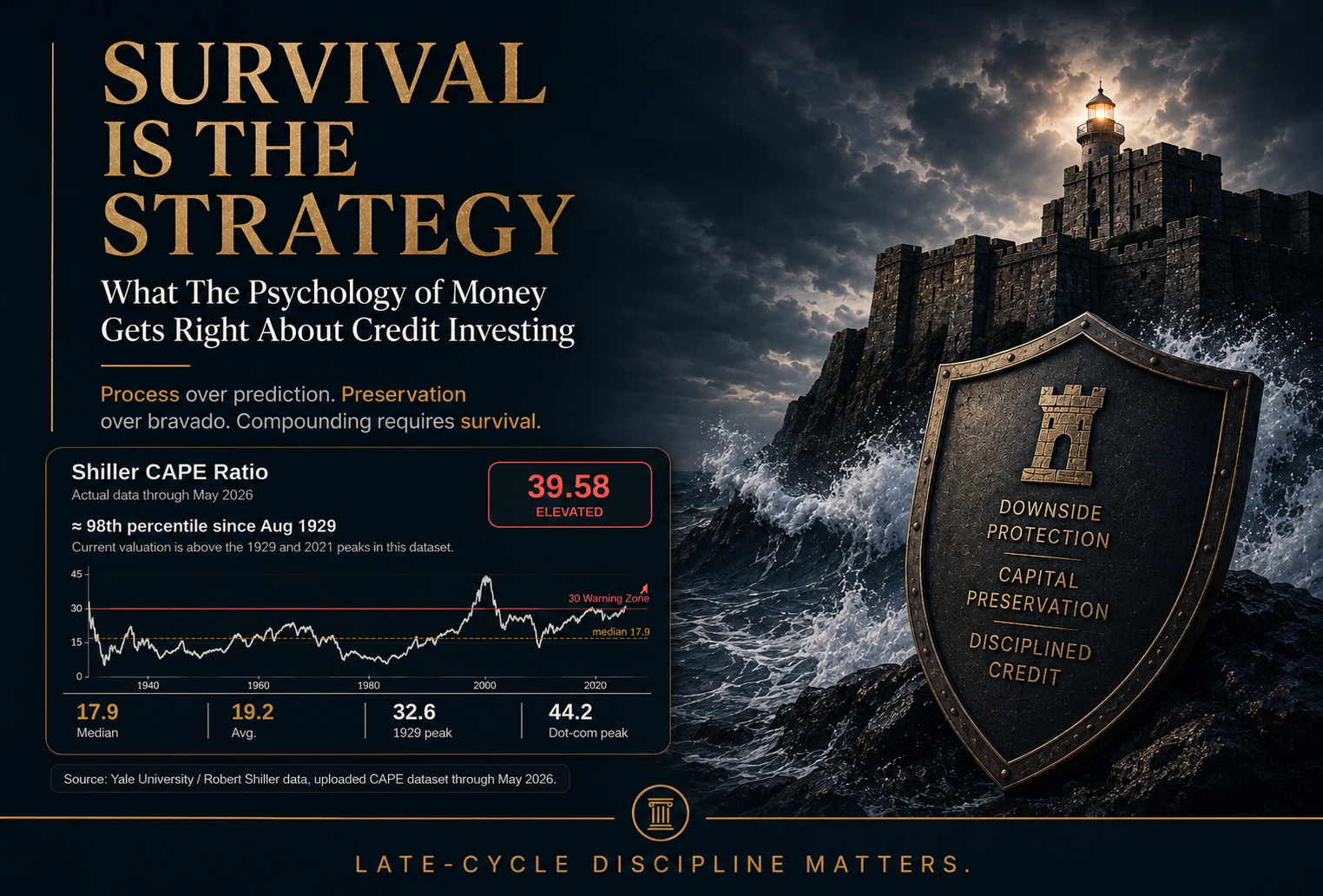

→ The Shiller CAPE ratio is hovering near 40, the second-highest reading in a century. The only higher print came at the peak of the dot-com bubble.

→ After that bubble burst, the S&P 500 took over 13 years to recover to break-even on an inflation-adjusted basis.

→ The ECY currently projects roughly 1.3% p.a. of real-return pickup for holding equities over Treasuries — against a 50-year median of 3.1%. To restore that median, the S&P 500 would need to be more than 40% below today's levels.

→ Berkshire Hathaway is sitting on a record cash pile of nearly $400bn. At the recent annual meeting, Warren Buffett made clear this is not his idea of an attractive investing environment.

Few investors have a repeatable, multi-decade record of being liquid into panic and deploying into dislocation. Buffett is one of them. When his cash position hits records, history suggests it is worth paying attention.

So the question stands: against a backdrop of geopolitical fragility and rising sovereign debt loads, are equity investors being paid enough to take the additional risk?

We don't believe so.

The relative-value disparity points clearly toward fixed income — and within fixed income, asset-based credit stands out.

Versus listed equities and traditional corporate debt, it offers higher yield premiums, contractual cash flows, the protection of real collateral, lower duration, orthogonal return streams, and a natural hedge against inflation.

For investors who have ridden the equity rally, this looks like a sensible moment to lock in profits and reallocate into a strategy built for resilience rather than reliance on continued multiple expansion.

The real question for your portfolio: is the equity risk premium enough today, or are markets pricing perfection?

.png)

.svg)