.svg)

Is Private Credit the New Subprime? No.

Over the past several months, investors have been inundated with headlines warning that “cockroaches” are lurking in private credit portfolios, a term Jamie Dimon used in October 2025 when discussing troubled loans tied to bankrupt companies such as Tricolor and First Brands. Some commentators have gone further, drawing comparisons between today’s private credit landscape and U.S. subprime in 2007.

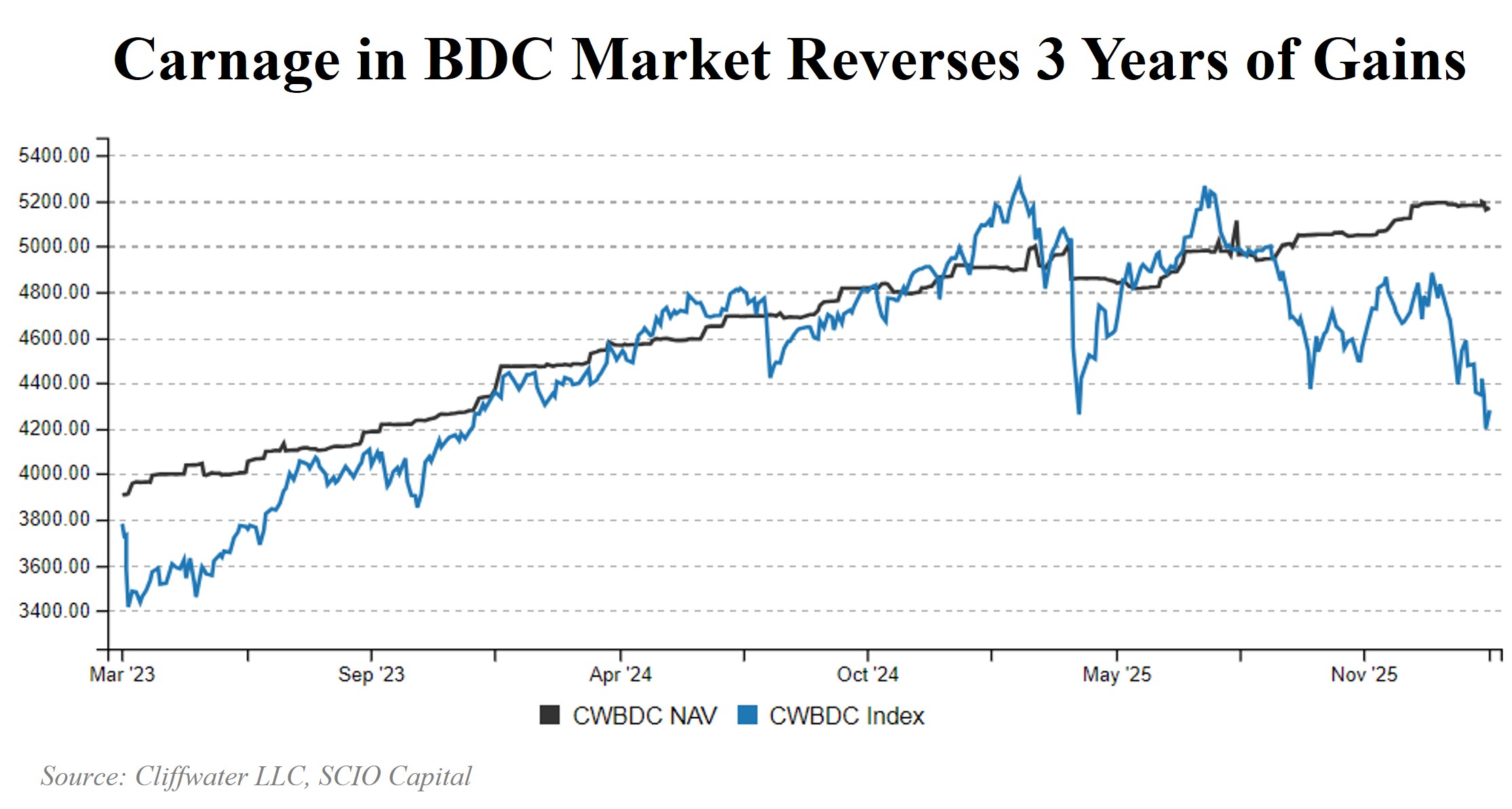

The result has been a sharp sector wide sell-off in Business Development Companies (BDCs)—publicly listed vehicles that originate and hold private corporate loans—with the Cliffwater BDC Index down roughly 19% year-on-year and BDCs, on average, trading around 18% below NAV.

To be clear: some of the criticism aimed at BDCs is fair.

Are some BDC portfolios meaningfully exposed to the tech sector? Yes.

Did some managers, in the scramble to deploy dry powder, agree to weaker covenant protections than they should? Also yes.

But the media is structurally optimized for attention, not salience, and the “private credit = subprime” comparison collapses under even basic scrutiny:

· BDCs predominantly hold senior secured, floating-rate loans, which typically sit higher in the capital structure, benefit from collateral packages, and provide lenders with more control rights than public high yield. Floating rates also help offset inflation and rate risk relative to fixed-rate debt.

· Systemic bank exposure is far lower. Private credit today is largely funded by asset managers, insurers, and pensions, with banks generally playing a smaller role as direct balance-sheet holders than they did in the pre-GFC mortgage machine.

And history is worth remembering. The last two times BDCs traded near an 18% discount to NAV—in 2020 and 2022—buyers were ultimately rewarded with substantial gains over the following 12 months.

So… are BDCs a buying opportunity at these levels?

With more than 30 years in structured credit markets, my answer is: “Which BDC?”

There is no single “BDC trade.” Each one is its own structure—effectively a managed credit vehicle—and its fundamental value depends on:

1. the underlying portfolio (credit quality, sectors, documentation, non-accruals, marks),

2. the leverage employed, and

3. the structure and governance (fees, incentives, liquidity tools, and how the manager behaves under stress).

Only after estimating fundamental value—often meaningfully different from reported NAV depending on assumptions—and comparing it to the market price can you form a real view on relative value.

In credit, the devil isn’t in the headlines. It’s in the documents.

.png)

.svg)